Gold and Silver Price Dynamics in Global and Vietnamese Markets

Precious Metals Markets

The precious metals market has experienced extraordinary volatility and growth in 2025, with both gold and silver reaching significant price milestones amid global economic uncertainty. This comprehensive analysis examines the 10-day price movements from August 26 to September 4, 2025, alongside current market conditions and projections for the remainder of the year, with particular focus on the unique dynamics within Vietnam’s precious metals market.

Current Market Overview: Record-Breaking Performance

Global Gold Market Dynamics

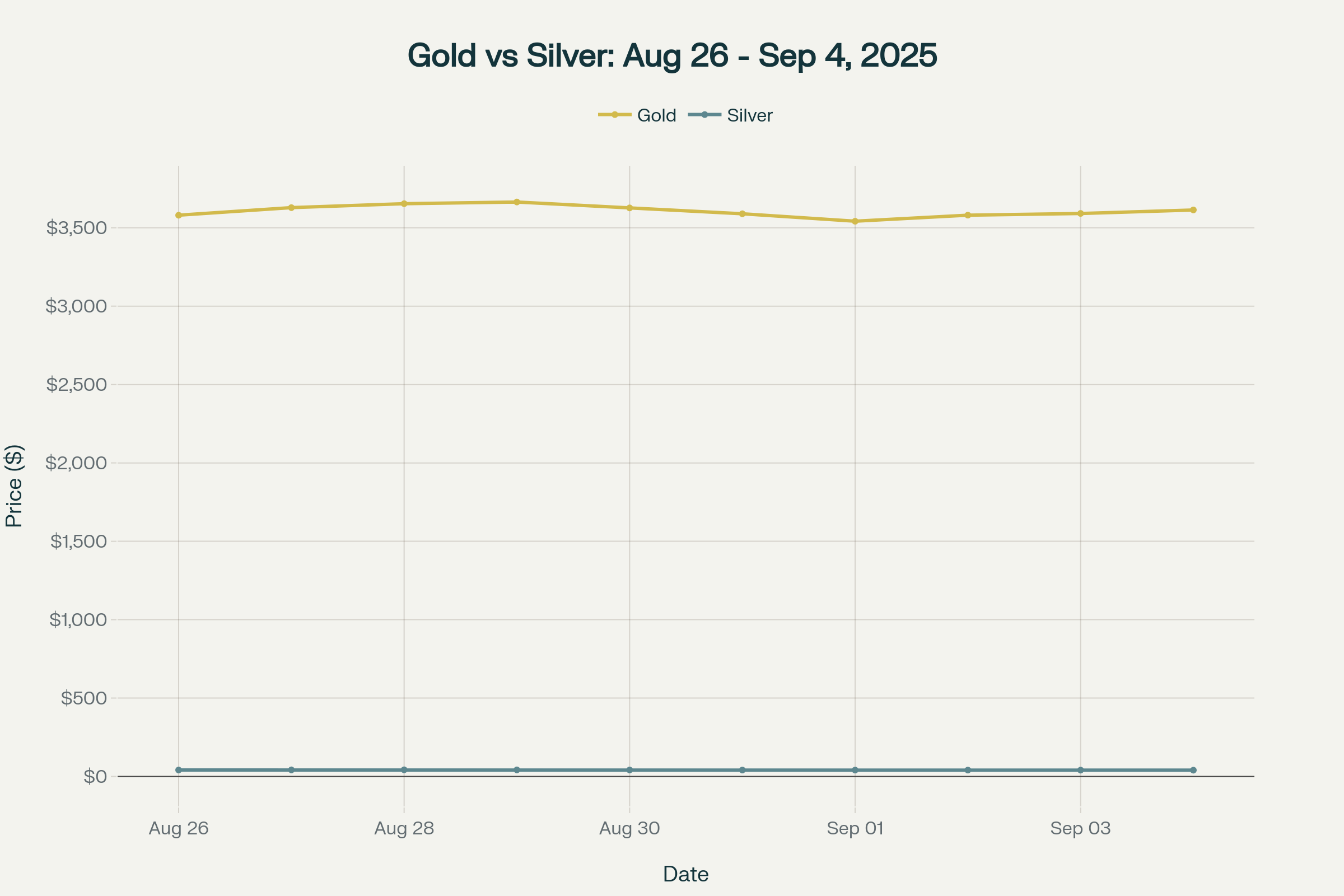

Gold has established itself as the standout performer in 2025, with prices surging +40.62% year-to-date to reach all-time highs above $3,580 per ounce. The precious metal closed at $3,605.80 on September 4, 2025, representing a slight decline of $29.70 from the previous session but maintaining its position near record levels. Over the analyzed 10-day period, gold demonstrated relative stability with a modest 0.95% increase, rising from $3,580.00 to $3,613.83 per ounce.[1][2]

The metal’s exceptional performance has been driven by a confluence of factors including Federal Reserve rate cut expectations, with market participants pricing in an 87% probability of a 25-basis-point reduction in September 2025. This monetary policy anticipation, combined with persistent geopolitical uncertainties and US dollar weakness – experiencing its worst annual start since 1973 – has created an ideal environment for gold appreciation.[2][3][4][5]

Silver’s Industrial and Investment Appeal

Silver has demonstrated even more impressive percentage gains, climbing +54.71% year-to-date from approximately $28.92 at the beginning of 2025. However, the 10-day analysis reveals greater volatility, with silver declining 2.30% from $41.00 to $40.06 per ounce during the examined period.[6][7]

Despite this short-term correction, silver maintains its position above $40 per ounce, a psychologically significant level that many analysts view as a foundation for further gains.[8][9]

The silver market continues to face structural supply deficits for the fifth consecutive year, with 2025 expected to show a shortfall of approximately 149 million ounces. Industrial demand, particularly from solar panel manufacturing and electric vehicle production, remains robust as China’s energy transition policies maintain momentum.[10][8]

Vietnam’s Unique Market Dynamics: Premium Pricing and Policy Changes

Significant Price Premiums

Vietnam’s precious metals market operates with substantial premiums above international prices, creating unique investment dynamics for local participants. Vietnamese gold prices currently trade at approximately VND 125-128 million per tael (roughly $4,100-4,200 per ounce), representing a premium of approximately $786 per ounce above global spot prices. This premium reflects the country’s historical state monopoly on gold production and import restrictions that have created supply constraints.[11][12][2]

Silver premiums in Vietnam are more modest, with prices around VND 32,863 per gram translating to approximately $42.40 per ounce, representing a $1.96 premium over international prices.[13]

The smaller silver premium indicates a more normalized market structure compared to gold.

Historic Policy Transformation

A pivotal development occurred on August 26, 2025, when the Vietnamese government issued Decree 232/2025/ND-CP, officially ending the 13-year state monopoly on gold bar production and raw gold imports. This landmark policy change, effective October 10, 2025, marks Vietnam’s transition from a state-controlled model to a regulated, competitive market structure.[14][15][16]

The decree allows commercial banks and eligible enterprises to obtain licenses for gold bar production, trading, and import/export activities. Market analysts expect this liberalization to gradually reduce the significant price premium, with projections suggesting the gap may narrow from the current VND 18-19 million per tael to approximately VND 7-8 million per tael over several months.[16][17]

2025 Price Projections: Bullish Consensus with Variance

Gold Price Forecasts: Targeting $4,000

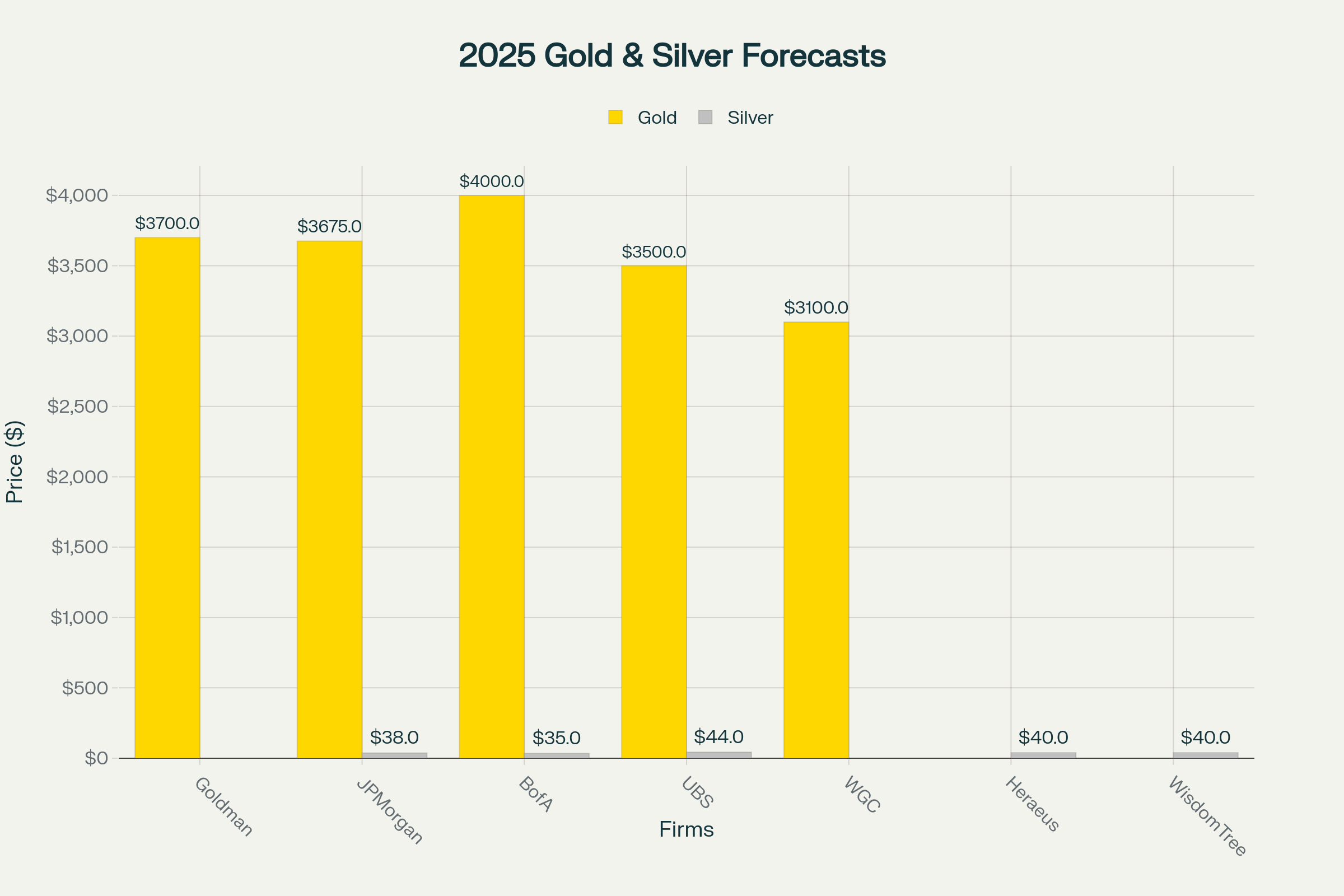

The investment community maintains a bullish consensus for gold through the remainder of 2025, with major financial institutions significantly revising their targets upward throughout the year. Goldman Sachs leads with the most aggressive forecast, raising their year-end target to $3,700 per ounce from a previous projection of $3,300. The investment bank cites continued central bank purchases averaging 80 metric tons monthly and increased ETF inflows as key drivers.[18][19]

JP Morgan provides an even more optimistic outlook, projecting gold to average $3,675 per ounce by Q4 2025, with prices advancing toward $4,000 per ounce by Q2 2026. The bank’s analysis emphasizes “tariff-driven recession and stagflation risks” as factors that will “continue to supercharge gold’s structural bull run”. Their sensitivity model indicates that every 100 tonnes of quarterly increase in investor and central bank holdings corresponds to approximately a 2% quarterly price increase.[20][18]

Bank of America anticipates gold reaching $4,000 by early 2026, while UBS maintains a more conservative $3,500 target for 2025. The World Gold Council suggests gold may trade sideways with a 0%-5% upward bias in the second half of 2025, though they acknowledge potential for 10%-15% additional gains if economic conditions deteriorate further.[4][19][21]

Silver Projections: Industrial Demand Driving $40+ Targets

Silver forecasts demonstrate greater variability but maintain a constructive outlook, with most analysts targeting the $35-44 range by year-end 2025. UBS provides the most bullish projection, maintaining official targets of $42-44 per ounce while outlining scenarios where prices could surge to $50 per ounce in the near term.[22][10]

JP Morgan projects silver reaching $38 per ounce by late 2025, while Heraeus Precious Metals expects trading in a $28-40 range, noting that silver remains undervalued relative to gold despite this year’s rally. WisdomTree forecasts silver reaching $40 per ounce by Q3 2025, representing a 17% increase from late October 2024 levels.[10][20][22]

The silver market’s dual nature as both a precious metal and industrial commodity creates unique dynamics. Industrial demand, particularly from photovoltaic applications, continues expanding as newer solar technologies require more silver per panel than older versions. China’s energy transition policies remain a significant driver, supporting sustained industrial demand growth.[10]

Market Drivers and Risk Factors

Bullish Catalysts

Monetary Policy Environment: The Federal Reserve’s anticipated rate cutting cycle represents a primary bullish catalyst, with lower interest rates reducing the opportunity cost of holding non-yielding precious metals. Market expectations of three rate cuts in 2025, beginning with a September reduction, support continued precious metals strength.[2][3][4][20]

Central Bank Demand: Global central banks are expected to purchase over 900 tonnes of gold in 2025, maintaining the structural trend of de-dollarization and reserve diversification. The Currency Composition of Official Foreign Exchange Reserves (COFER) data shows continued, albeit moderate, diversification away from US dollar holdings.[4][20]

Geopolitical Uncertainties: Ongoing conflicts, trade tensions, and policy unpredictability continue supporting safe-haven demand. The potential for tariff implementations and trade disruptions creates additional uncertainty that typically benefits precious metals.[23][5][4]

Supply Fundamentals: Silver’s structural supply deficit and limited gold mine production growth provide fundamental support for higher prices. Industrial silver demand growth, particularly from renewable energy and automotive sectors, continues outpacing supply increases.[8][10]

Potential Risk Factors

Valuation Concerns: Current price levels create vulnerability to corrections, particularly if economic conditions improve more rapidly than expected. Gold’s 26% year-to-date gain through the first half of 2025 suggests potential for consolidation periods.[4][24]

Policy Changes: Unexpected shifts in Federal Reserve policy or resolution of major geopolitical conflicts could reduce safe-haven demand. Additionally, Vietnam’s market liberalization may lead to premium compression faster than anticipated, affecting local pricing dynamics.[17][4]

Technical Indicators: Some analysts note that recent strong rallies may require consolidation periods to establish sustainable foundations for further advances. VanEck suggests investors should “be prepared for a slight pullback in the near term given its significantly strong run recently”.[24][4]

Vietnam Market Outlook: Normalization and Opportunity

Short-Term Transition Period

The implementation of Vietnam’s gold market liberalization will likely create short-term volatility as market participants adjust to new supply dynamics. Analysts expect the registration and approval process for gold import and production to require 2-3 months before meaningful supply increases reach the market.[17]

Market psychology shifts are already evident, with buyers no longer maintaining a “buy at all costs” mentality while existing gold holders consider profit-taking opportunities. This behavioral change may help ease market tension even before official new supply enters the market.[17]

Long-Term Structural Changes

The premium reduction process is expected to be gradual rather than immediate, with the current VND 18-19 million per tael premium potentially declining to VND 7-8 million per tael over several months. Complete market normalization may require 6-12 months as supply chains establish and market participants adapt to competitive dynamics.[17]

Silver markets in Vietnam are expected to experience less dramatic changes due to smaller existing premiums and different supply dynamics. The industrial applications of silver may create more stable demand patterns compared to gold’s investment-driven volatility.[13]

Conclusion: Navigating a Transformative Market Environment

The precious metals market in 2025 represents a convergence of extraordinary circumstances: record-high prices driven by monetary policy expectations, persistent geopolitical uncertainties, and structural supply-demand imbalances. Both gold and silver have demonstrated remarkable year-to-date performance, with gold gaining over 40% and silver advancing more than 54%.[1][6]

The 10-day analysis period reveals the characteristic volatility of precious metals markets, with gold showing relative stability (+0.95%) while silver experienced greater fluctuation (-2.30%). These short-term movements occur within the context of a longer-term bull market that most analysts expect to continue through 2025 and potentially beyond.

Vietnam’s market transformation represents a unique opportunity for both local and international participants. The end of the state monopoly system should gradually normalize pricing dynamics while potentially maintaining Vietnam’s position as a significant regional precious metals market. The transition period may create both opportunities and risks as premiums compress and supply patterns establish new equilibrium levels.

Looking forward, the consensus forecast range of $3,500-4,000 for gold and $35-44 for silver by end-2025 reflects continued optimism tempered by recognition of current elevated valuations. The success of these projections will largely depend on Federal Reserve policy execution, geopolitical developments, and the pace of global economic recovery.[19][22]

Investors should prepare for continued volatility while recognizing the structural factors supporting precious metals: ongoing monetary accommodation, central bank buying programs, industrial demand growth for silver, and persistent economic uncertainties. Vietnam’s market evolution adds an additional dimension of opportunity as premium compression creates potential value adjustments in one of Asia’s most significant precious metals markets.